No V, No Victory

For years every dip meant victory. Now the market keeps drawing something else.

Throughout V for Vendetta, the mysterious figure known only as V leaves his mark everywhere he goes.

A symbol, not of chaos. But victory. Signaling that even something as broken as the establishment can still be overturned.

Markets used to believe in that kind of victory too.

Ever since bottoming in October 2022, every selloff carried the same expectation: sharp drop… sharp rebound… back to new highs.

A clean, confident V-shaped recovery. Blink and you’d miss the dip.

But lately?

That symbol has gone missing.

Instead of decisive recoveries, we’re getting hesitation. Failed breakouts. Choppy rotations. Weak breadth. New lows.

The market still remembers what a V looks like.

It just isn’t drawing one anymore.

And when a symbol that powerful stops appearing, it’s usually worth asking why.

More than Oil

Whilst the S&P 500 struggles near multi-month lows, geopolitical tensions are pushing toward multi-year highs. That’s no coincidence.

But despite everything unfolding in the Middle East and oil surging back toward levels last seen in 2022, I’m not entirely convinced the moves we’re seeing across markets can be laid solely at Iran’s feet.

Take a look at the price action in SPY over the past five months.

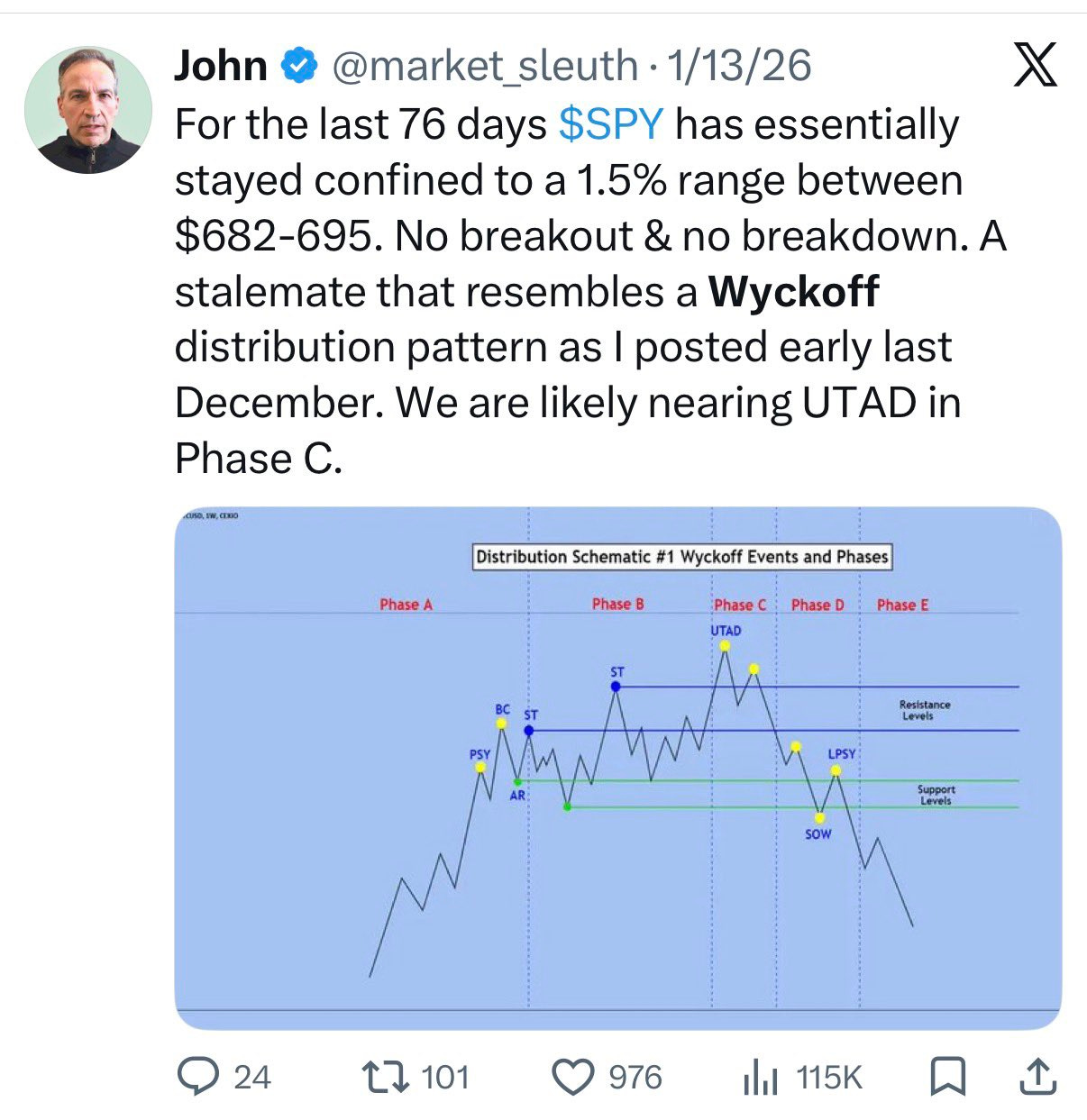

After printing fresh highs in October, the index quickly shed around 5% in early November before settling into a choppy, sideways range - repeatedly failing to break above the 1.618 Fibonacci extension of the move from the April lows to the prior highs at $693.50.

As I noted before the recent drop, the longer price stayed trapped in this structure, the more it began to resemble a classic Wyckoff Distribution pattern.

It wasn’t just me seeing it either - my friend John friend flagged the setup on X as it was forming (way before I did), much to the irritation of the usual troll accounts who only ever seem to recognize risk once it’s already priced in.

Which brings me back to my original point.

If the current drawdown is due to the conflict in Iran, then why were markets holding a clear Wyckoff Distribution pattern for the four months prior to the attacks?

For Clues, Observe the Tape

We can all speculate when answering this question: private credit stress, labour market weakness, positioning, profit-taking. But where’s the skill in that?

Personally, I’m not ashamed to admit I don’t know the reasons - but do I need to?

When it comes to analysing markets, the tape usually tells you what matters long before the headlines do.

And in hindsight, some of the clearest warnings were hiding in plain sight.

Bitcoin rolled over first.

Not exactly the behavior you’d expect from the market’s favorite liquidity barometer if risk appetite was healthy beneath the surface.

Financials followed.

Even more concerning. Because when banks start struggling, it’s rarely about geopolitics - it’s usually about something closer to the plumbing of the system.

Put simply: if this selloff were purely about Iran, we wouldn’t expect to see some of the most liquidity-sensitive and credit-sensitive corners of the market weakening months in advance.

So Wen V?

As alluded to in the intro, what’s most notable to me right now is the absence of V-shaped recoveries across the board. From 2024’s Yen Carry Trade to last year’s tariff tantrum, ‘the V’ always stepped in to save the bulls…

But that playbook only works when the same leadership groups that took us down are the ones snapping back higher. And right now, they aren’t.

In fact, they’re doing the opposite - and completing what looks to be massive tops.

HYG, completing a top.

QQQ, completing a top.

SPY, completing a top.

Bitcoin, looking like it wants lower…

What About a Ceasefire?

You don’t have to look far to see traders speculating about what happens if - or when - a ceasefire deal is reached between the United States, Israel and Iran.

On the surface, the reaction feels obvious.

A ceasefire would likely send SPY sharply higher.

Oil would probably fall as the geopolitical risk premium unwinds. Inflation expectations would ease at the margin. Volatility would compress. And just like that, the narrative would flip back to risk-on almost overnight.

Markets typically respond positively to reductions in uncertainty, especially when oil prices retreat after conflict-driven spikes. In other words: the conditions for a classic headline-driven rally would be there.

But here’s the problem.

Not every rally is a V-shaped recovery.

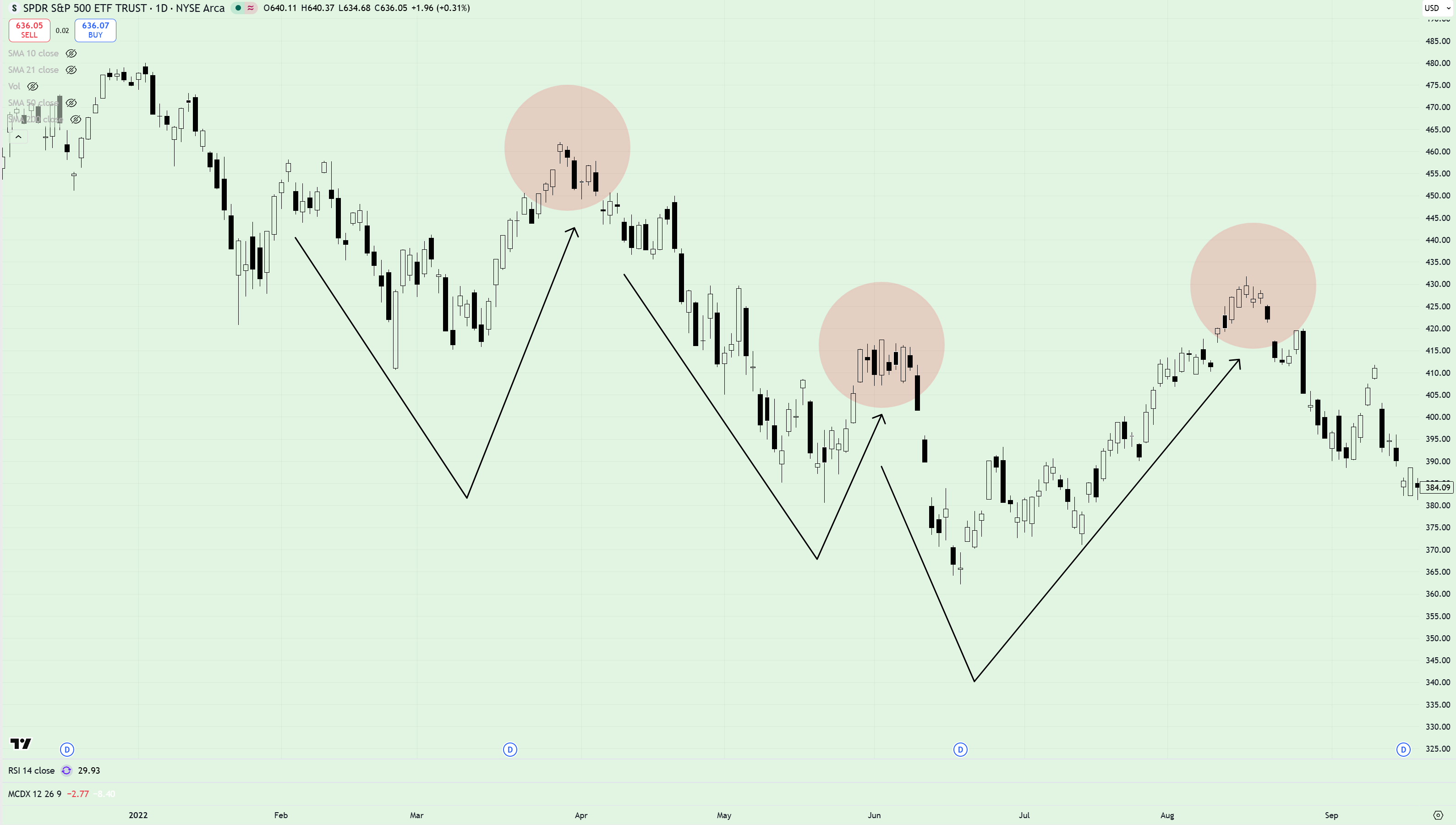

Just look at how these so-called ‘V’ recoveries played out between 2021 and 2022.

Each time, buyers were pulled back in just as price started to stabilise - only for SPY to roll over again and make fresh lows. Every bounce exhausted another wave of dip-buyers before the market finally carved out a durable bottom in October 2022.

That’s the pattern I’ll be watching for if we see a bounce from current levels.

Not a reason to load the boat. But potentially an opportunity to fade the pop.

Because if this market is going to produce a real V - the kind we became used to after every scare between 2020 and 2024 - then the leadership that broke first needs to recover.

That means:

HYG needs to stabilise.

Credit doesn’t fake strength for long. If high yield continues to lag, risk appetite isn’t actually returning. The same goes for Bitcoin and broader crypto.

XLF needs to rally.

Banks don’t sit quietly in the corner during healthy recoveries. If financials stay weak, something in the plumbing is still under pressure.

XLY needs to outperform.

Consumers lead expansions. They don’t confirm them after the fact.

The longer each of these remain pinned beneath clear and obvious topping structures, the harder it becomes to argue that any bounce in the index represents victory rather than relief.

In other words:

Until the generals turn higher, it’s dangerous to trust the army.

Best,

Alex