Order, Order!

The Market Vs The People

12 Angry Men is an awesome film.

A classic courtroom drama set almost entirely inside a jury room, twelve jurors must decide the fate of a teenage boy accused of murdering his father.

At the start, eleven jurors are ready to declare him guilty without much discussion — except for one, Henry Fonda, who isn’t convinced.

Saving those of you that haven’t seen the film from any potential spoilers, I won’t divulge what plays out.

Instead, I’ll simply liken my current stance to that of Fonda’s - skeptical, whilst those around me have already voted ‘bullish’ without a second look at the evidence.

The Defense States its Case

Since the April lows the bulls have presented an impeccable case.

From QQQ to SPY, Bitcoin and High Beta, higher lows and higher highs have pushed the market to all time highs at a relentless pace.

Everything from key moving averages to volume have confirmed these moves too - with earnings season underpinning the trend with solid growth across all areas you’d expect to see in a bull market: tech, discretionary, high beta etc.

Elsewhere, all the usual trends you’d expect to see in the market have been supporting the bulls. Just take a look at XLP relative to XLY since the April lows - pinned below a downward sloping 50dma, breaking down to new multi-year lows.

And it’s a similar look when comparing TLT relative to SPY - again, multiyear lows.

And Now, The Prosecution

Given the weight of evidence that’s been presented over the summer, it’s difficult to imagine a scenario in which the bears could overturn this particular case.

And yet over the last few weeks, the prosecution has been steadily preparing its files and gathering evidence.

Let’s start with Exhibit A, Bitcoin.

Since breaking to new highs in early October, Bitcoin has traded like a dog, recently falling below its 50wma for the first time since 2021.

On shorter timeframes, not only does Bitcoin look weak, SOL and ETH have been having a torrid time too, dropping below the anchored VWAP from the April lows and flipping it from support to resistance. Here’s ETH for context:

How does this relate to equities?

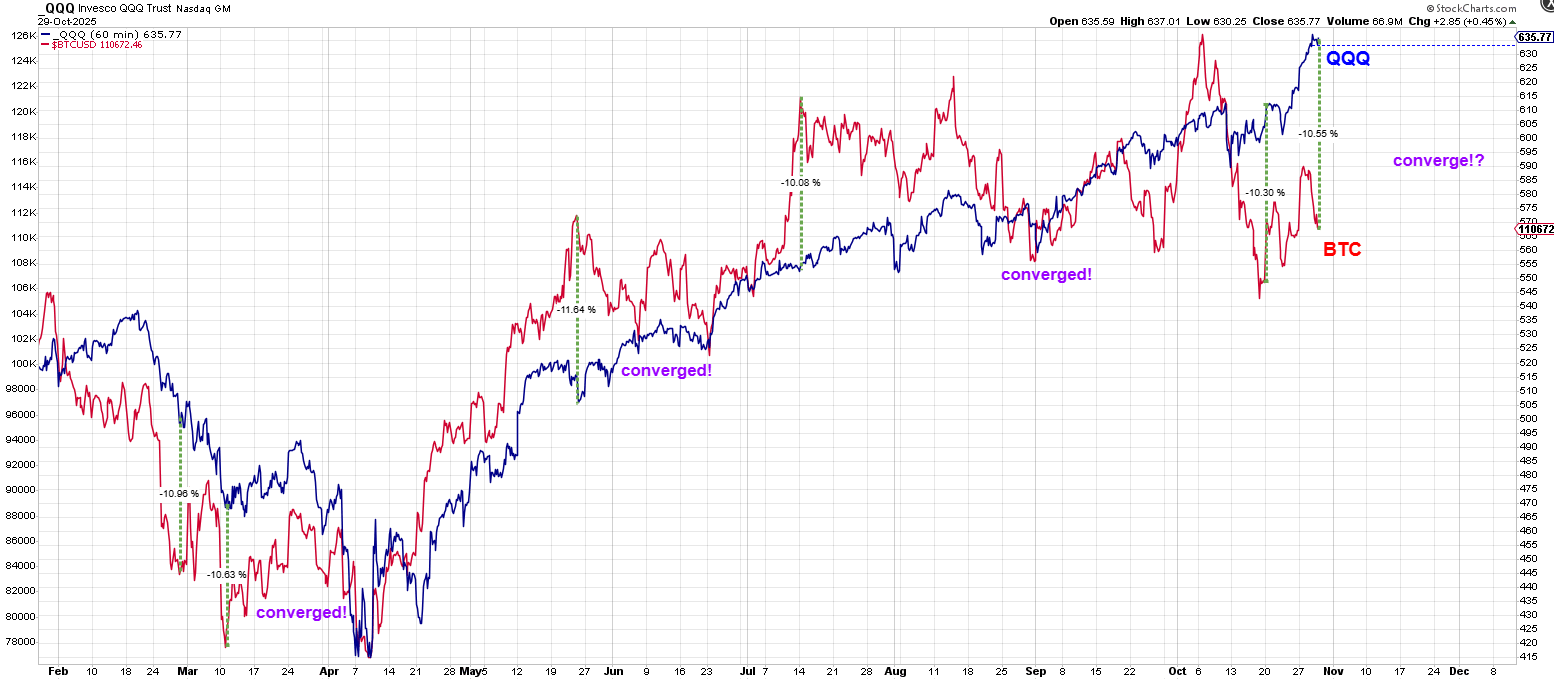

Let’s start with the correlation between QQQ and BTC.

These two have traded in lockstep for the best part of three years - but have now diverged. And whilst it’s possible that Bitcoin catches up to QQQ here, given the weight of evidence discussed, that seems like hopium at best.

Credit to Heisenberg for the awesome chart work.

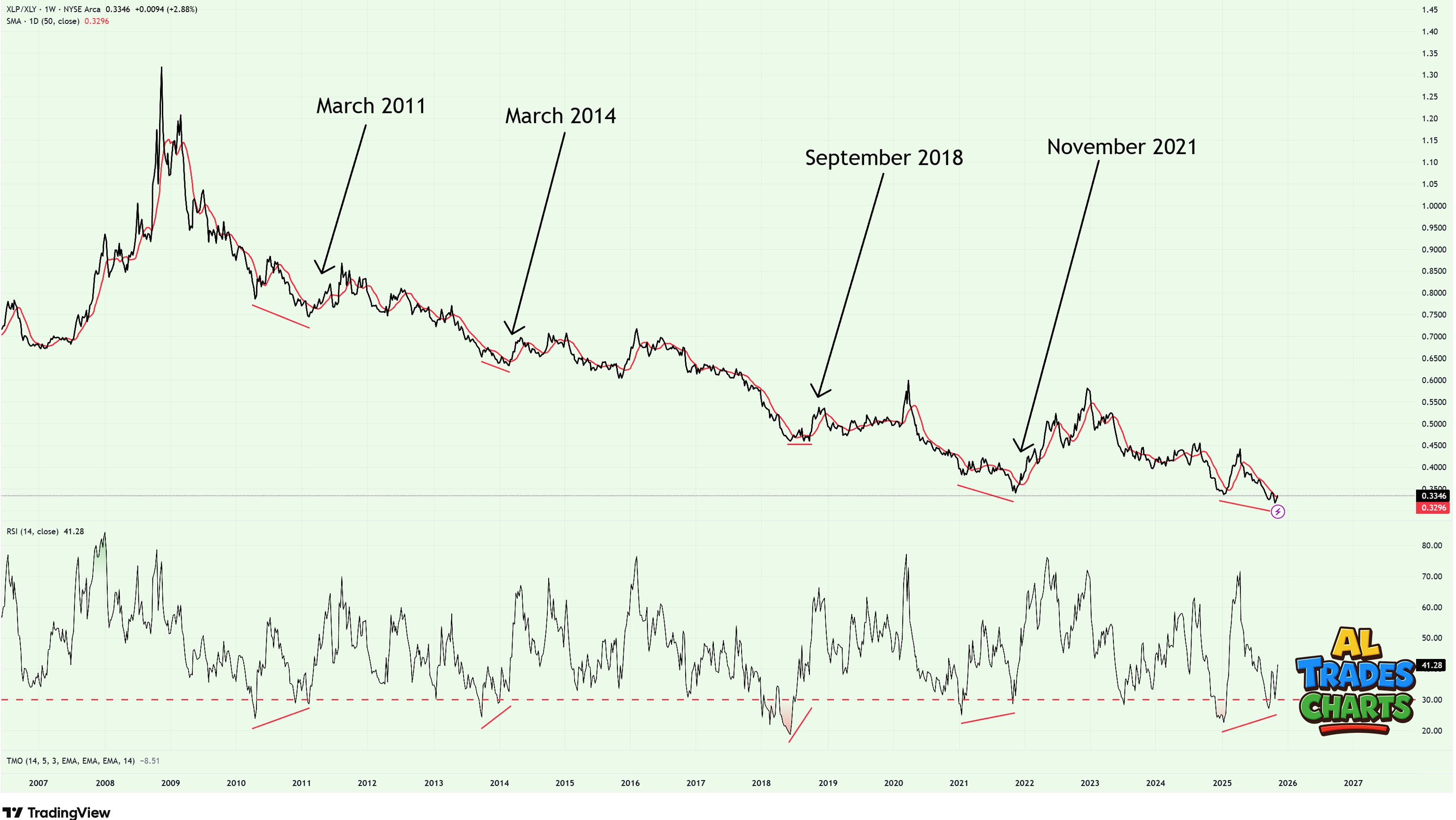

Next up, Exhibit B. XLP/XLY

Last week XLP relative to XLY reclaimed the 50dma following a bullish RSI divergence from oversold levels on the weekly chart. This is rare, with only four prior occurrences dating back to 2007.

Here’s what SPY did after each signal was fired:

March 2011: SPY would go on to make a new high in April before dropping 21% through October.

March 2014: SPY would go on to make a new high in May before losing 14% through January the following year.

September 2018: marked the local top. SPY fell 20% before bottoming in December.

November 2021: SPY would go on to make a new ATH in January before dropping 27% through October 2022.

Long story short - should SPY make a new high (which I’m definitely not ruling out in the short term) I’ll be treating it with caution rather than blind exuberance.

Especially if XLP/XLY continues to hold above its 50dma.

And Lastly, Exhibit C. Breadth.

If you’re an active trader like me, you’re probably already aware of breadth deterioration and are sick of hearing about it, so I’ll keep this section short and sweet.

The key point to understand here is that the percentage of SPX stocks trading above their respective 20dma, 50dma and 200dma peaked in Q2 and have been making lower highs and lower lows ever since.

Adding to these concerns, we’re also seeing short term breadth improvements on defensive components such as energy and staples, whilst prior market leaders - tech, discretionary - have been showing signs of exhaustion on similar timeframes.

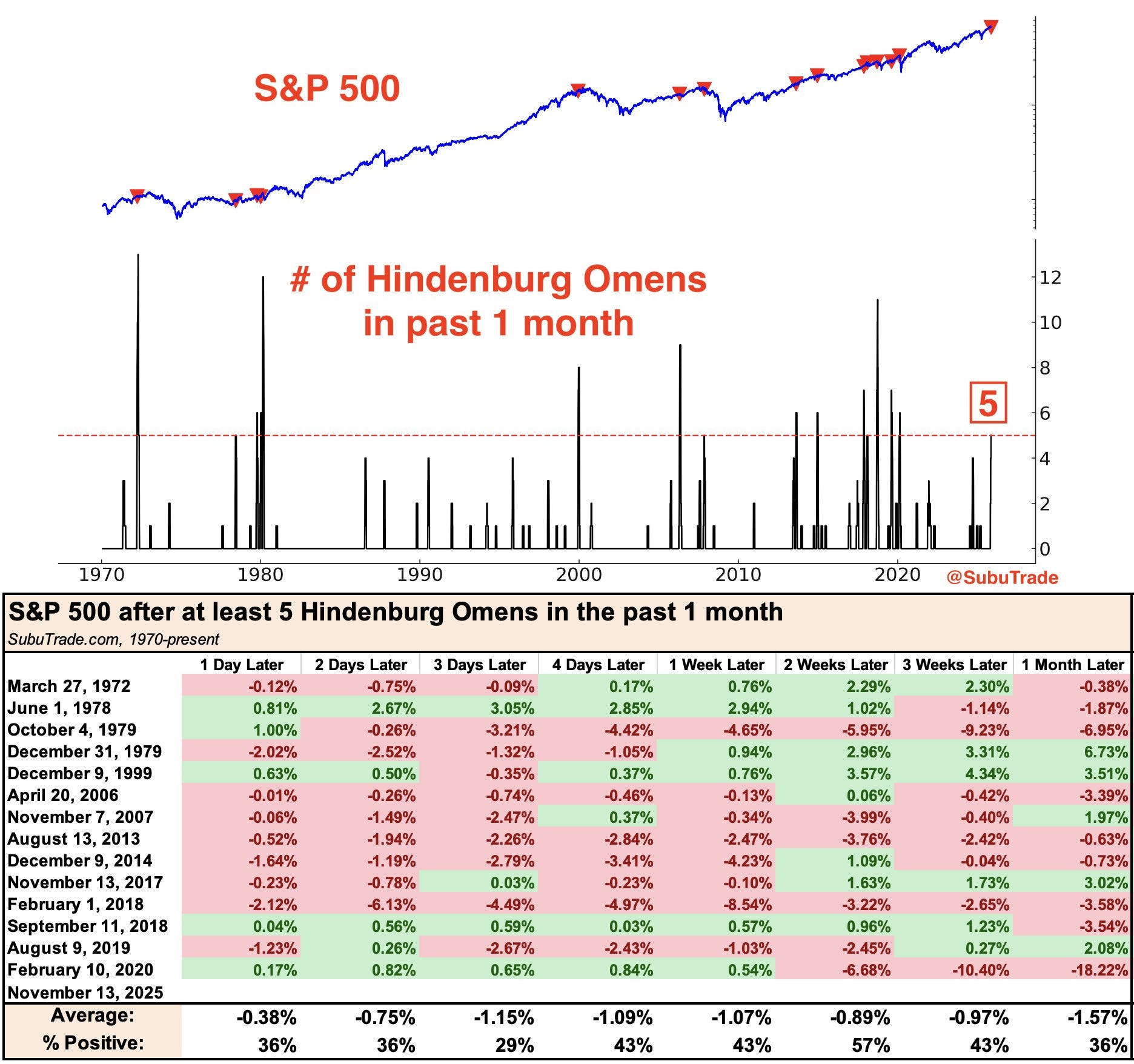

And lastly, we’ve had not one but five Hidenburg Omens in the last month.

Courtesy of the excellent Subu Trade, here’s what prior signals meant for the S&P 500 in the month that followed at least 5 Hindenburg Omens:

The Verdict (For Now)

Just like in 12 Angry Men, we’ve heard two sharply different arguments.

On one side, the defence: powerful trends, strong earnings, pristine technicals and a market that — from April until recently — has behaved exactly as a bull market should.

On the other, the prosecution: crypto rolling over, defensive ratios flashing historically rare signals, breadth deteriorating and a cluster of Hindenburg Omens that, at the very least, suggests pockets of instability beneath the surface.

And here’s where I land.

I’m not declaring the market “guilty.”

I’m not calling for a crash.

I’m not even saying the trend is definitively over.

But like Fonda in that jury room, I am saying this: the evidence no longer feels unanimous.

We’re at a point where the dominant narrative (”everything is fine, new highs are guaranteed, carry on”) deserves a second look.

This week I’ll be keeping my powder dry ahead of Nvidia earnings (Wednesday) and a key jobs report (Thursday). After that, we should get some clarity in regards to which way the jury’s leaning.

Have a great week.

Best,

Al