Peak Hawkishness?

Mega-caps say rate hikes. Bonds and biotech aren't so sure.

When Kevin Warsh stepped away from the mic after his FOMC presser debut, the sound of traders desperately typing out their ‘quick takes’ filled the Twittersphere.

While some interpreted the presser as hawkish, others celebrated the new chair’s ambiguous stance relating to forward guidance - something echoed by none other than the US Treasury Secretary, Scott Bessent.

Similarly, the market has been sending mixed signals as it digests the presser.

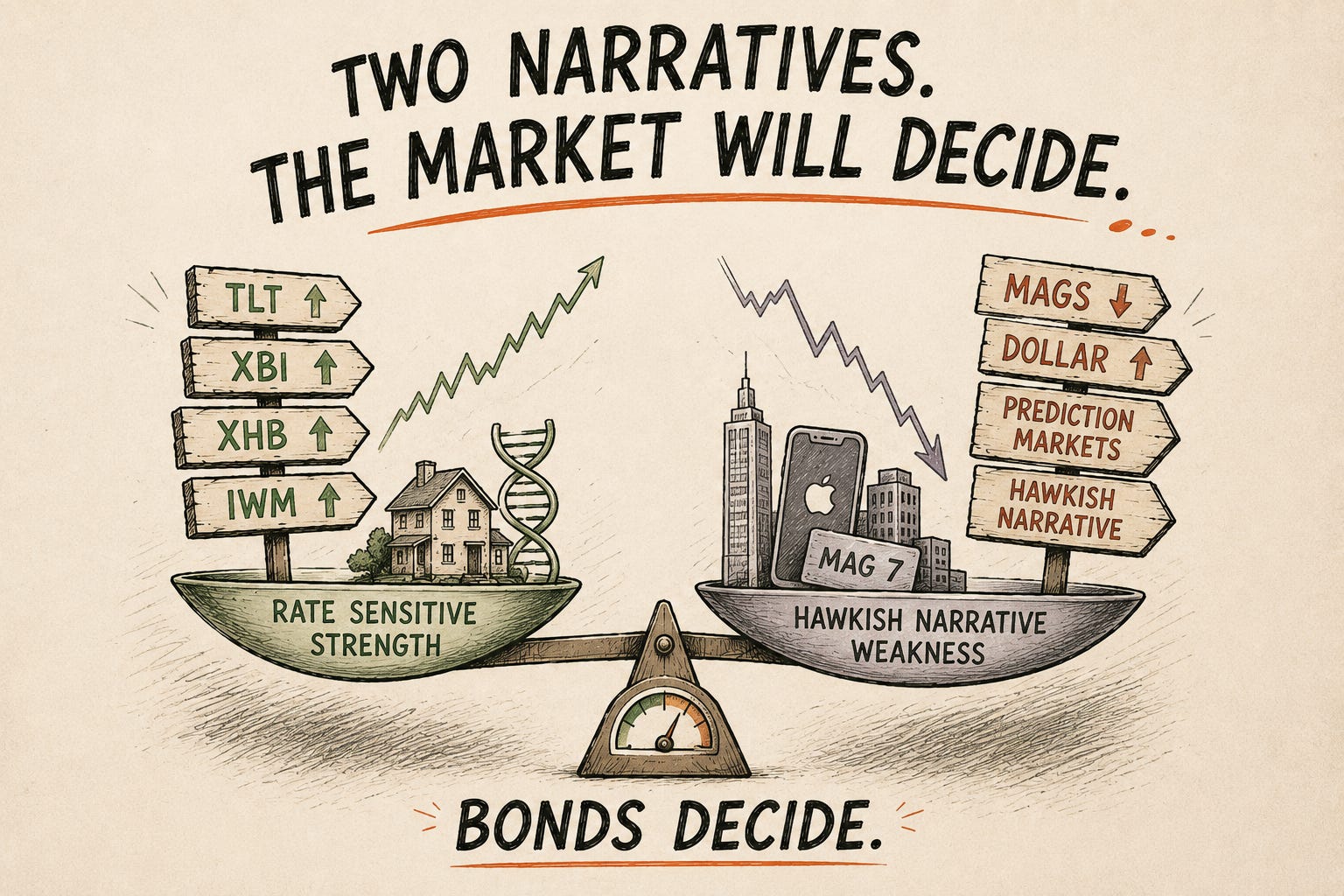

Mega cap tech is siding with the hawks. Bonds, biotech, homebuilders and small caps...not so much.

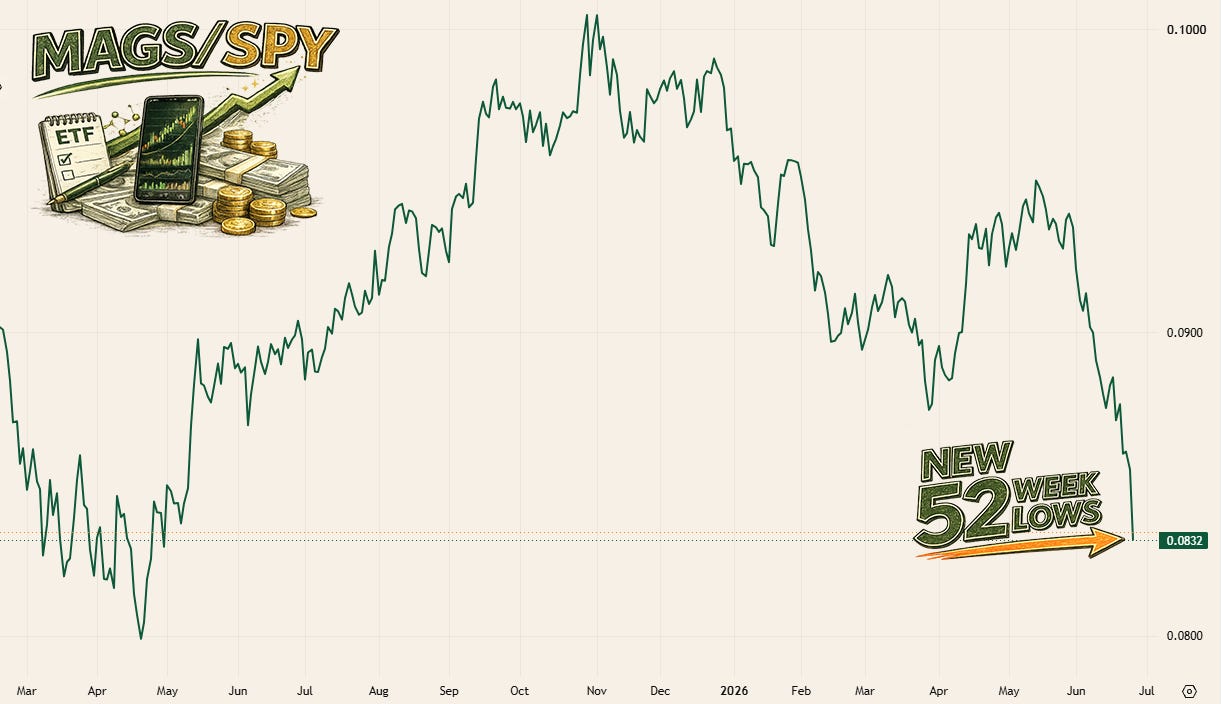

MAGS Signal Weakness

On the surface, it’s easy to understand why the market has become increasingly hawkish.

Since Warsh’s debut, MAGS has slipped below its 200-day EMA for the first time since April, while all seven constituents traded beneath their respective 50-day moving averages during the weekly session.

Relative performance looks even worse.

MAGS/SPY has registered fresh 52-week lows in four of the six sessions since the FOMC meeting, prompting traders to jokingly rename the ‘Mag 7’ the ‘Lag 7’.

Who said originality was dead?

Sure, taking the relative performance of MAGS and indeed the S&P500 - and to a lesser extent, the Nasdaq - in isolation, it’s easy to see why so many traders have attached themselves to the popular narrative that rate hikes, rather than rate cuts, are becoming ever-more likely in H2 2026 through H2 2027.

Prediction markets have embraced the same view. At the time of writing, Kalshi assigns an 81% probability of rate hikes before 2028, with a 65% chance the first arrives as early as July next year.

Sure, if you only looked at mega-cap tech, you’d probably reach the same conclusion.

The problem?

The rest of the market isn’t telling the same story

The Market Disagrees

Earlier this week I shared some thoughts on what I felt was a confusing tape.

On the one hand, mega cap weakness and a strengthening dollar. On the other, the incredible strength displayed by biotech stocks (XBI) and small caps (IWM).

Since then, I've spent some time digging into the data. The more I look, the less convinced I am by the market's prevailing hawkish narrative.

Here's a quick recap of what's happened since the FOMC press conference (in no particular order):

After closing at 4.95% on the day of the press conference, the 20-year Treasury yield has fallen to 4.87% (an 8 bp decline), while TLT is threatening a breakout above its 200-day EMA.

XBI has closed at fresh all-time highs every session since June 17, showing persistent leadership from one of the market’s most duration-sensitive groups.

IWM has held both its 10- and 20-day EMAs, registering three new intraday highs over the past five sessions.

XHB has broken to multi-month highs and remains firmly above its 10-, 20-, 50- and 200-day EMAs.

XLI has printed another all-time high and continues to trade well above a bullish moving average ensemble.

Here’s a question I can’t shake:

If Warsh had genuinely delivered a hawkish surprise, why are some of the market’s most rate-sensitive areas continuing to lead?

Traps Are Being Set

Right now, the tape appears to be setting traps in both directions.

Mega-cap weakness and a stronger dollar are tempting investors into a more hawkish interpretation, while beneath the surface, money continues to rotate into some of the market's most rate-sensitive areas, keeping the ‘peak hawkishness’ thesis in play.

These two messages rarely coexist for long. At some point, one camp is going to be left red-faced as the tape tears apart their carefully constructed, comfortable narrative.

Who wins?

In my view, bonds decide.

If the prevailing narrative proves correct and further rate hikes begin to enter the conversation, it’s difficult to argue against equities facing increasing headwinds.

The last time TLT experienced a sustained drawdown- 2022 being the obvious example- SPY entered a bear market, ultimately falling roughly 27% from peak to trough across a 12 month period.

But what if that doesn’t happen? What if the ‘long DXY, short TLT’ trade is over crowded? What if Warsh, isn’t as hawkish as everyone believes him to be?

A Quick Word on Warsh

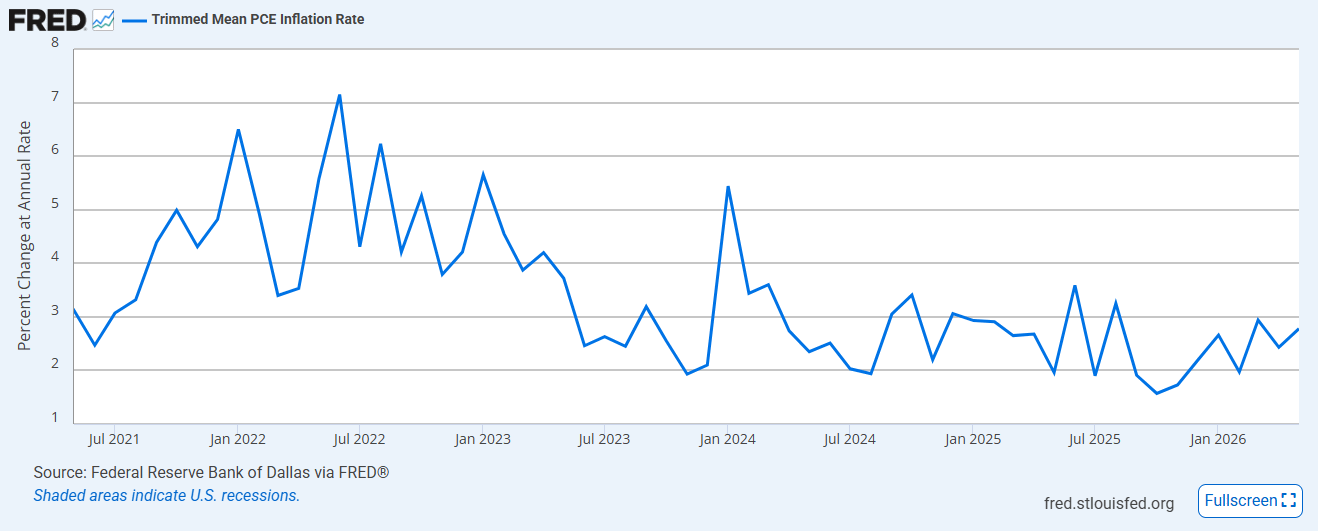

One inflation metric I'll be paying particularly close attention to over the coming months is Trimmed Mean PCE- the measure Kevin Warsh has repeatedly highlighted as his preferred gauge of underlying inflation.

Like headline CPI and core PCE, it's still moving in the wrong direction, reinforcing the market's increasingly hawkish interpretation of recent data.

That said, it's worth remembering that inflation is inherently backward-looking.

With tensions between the US and Iran easing and the risk of a sustained energy supply shock appearing to fade, it's not unreasonable to expect some of the recent inflationary pressure to unwind in the months ahead.

Therefore, should this metric begin to cool, it could provide a more compelling signal than CPI alone that underlying inflation isn’t the existential threat many argue it to be today, potentially reopening the door to a more accommodative Fed and, in turn, a more supportive backdrop for risk assets.

So What’s The Trade?

Assessing the weight of the evidence is part and parcel of being a trader. Right now, that means keeping a close eye on names and sectors that should be most sensitive to a changing rate environment, namely IWM, XBI, XHB and TLT.

Sure, we may continue to see the market shake out below its shorter-term moving averages. SPY and QQQ may even lose their 50-day EMAs. But in isolation, I’m not convinced that tells us much beyond the market taking a well-earned breather after a strong run.

If, however, the selling begins to broaden out and those rate-sensitive areas start rolling over alongside the major indices, then the weight of the evidence shifts - and with it, the outlook.

For now though, the tape remains choppy rather than broken. No need to panic. No need to rush in.

With that in mind, I’m happy to stay patient, let the data come to me, and adjust my positioning as the evidence evolves.

Have a great weekend.

Best,

Al