The Curb-Stomp Rally

What happens next is truly violent...

There’s a scene in American History X that everyone remembers. The curb stomp.

It comes after Derek’s car is broken into by three black men late at night. Fueled by rage and his deep involvement in a local neo-Nazi gang, he confronts them outside his house. He shoots two of them as they try to flee, then drags the third to the pavement.

What happens next is truly violent.

Derek calmly orders the man to bite down on the curb, pauses long enough for the audience to understand what’s about to happen, and then stomps on his head. The scene is filmed in stark black-and-white, heightening a sense of moral coldness and inevitability.

The reason the scene sticks isn’t just the violence. It’s the finality of it. One moment where resistance disappears and the outcome becomes obvious to almost everyone watching.

And over the last two weeks, markets delivered their own version of that very moment.

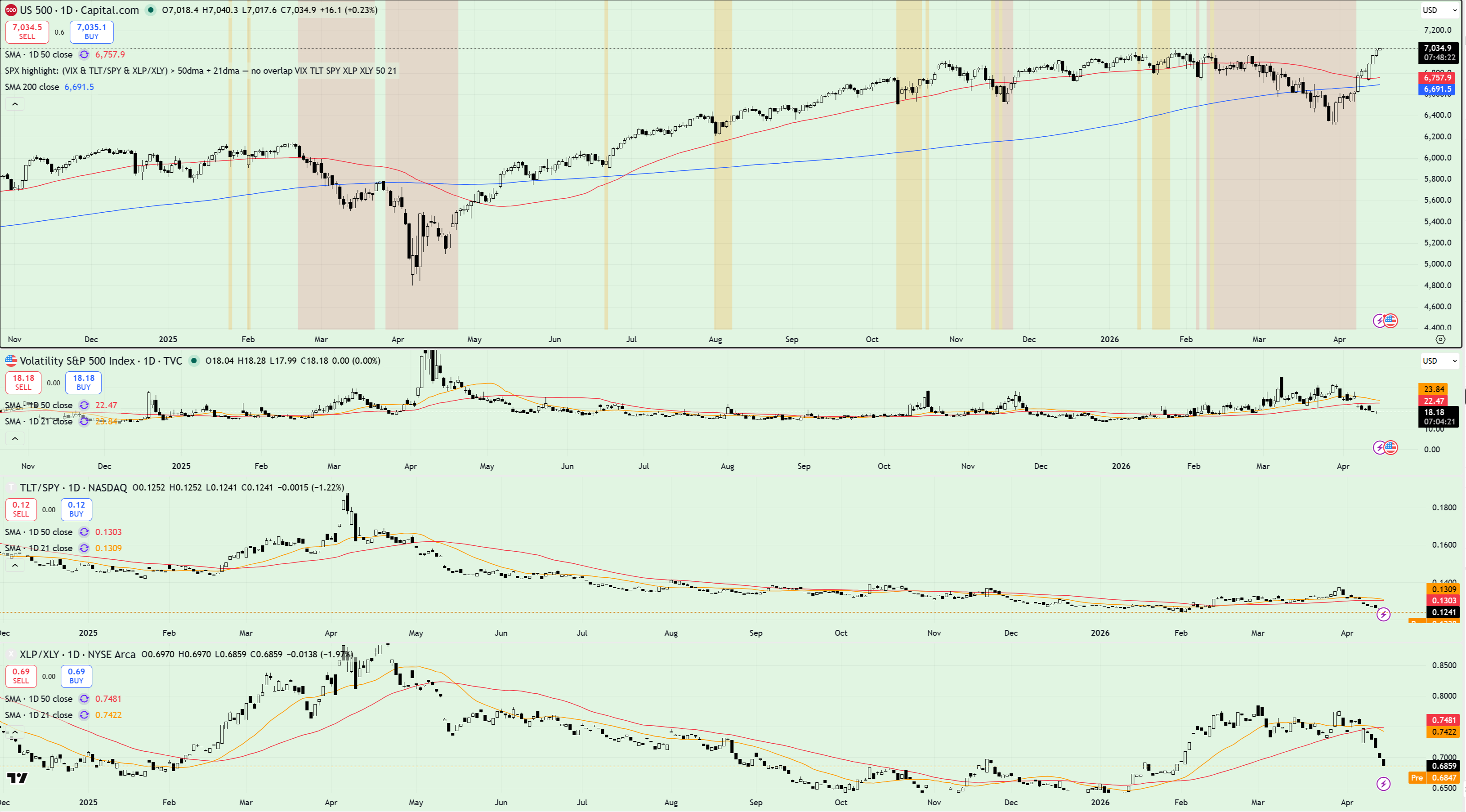

Here’s SPY.

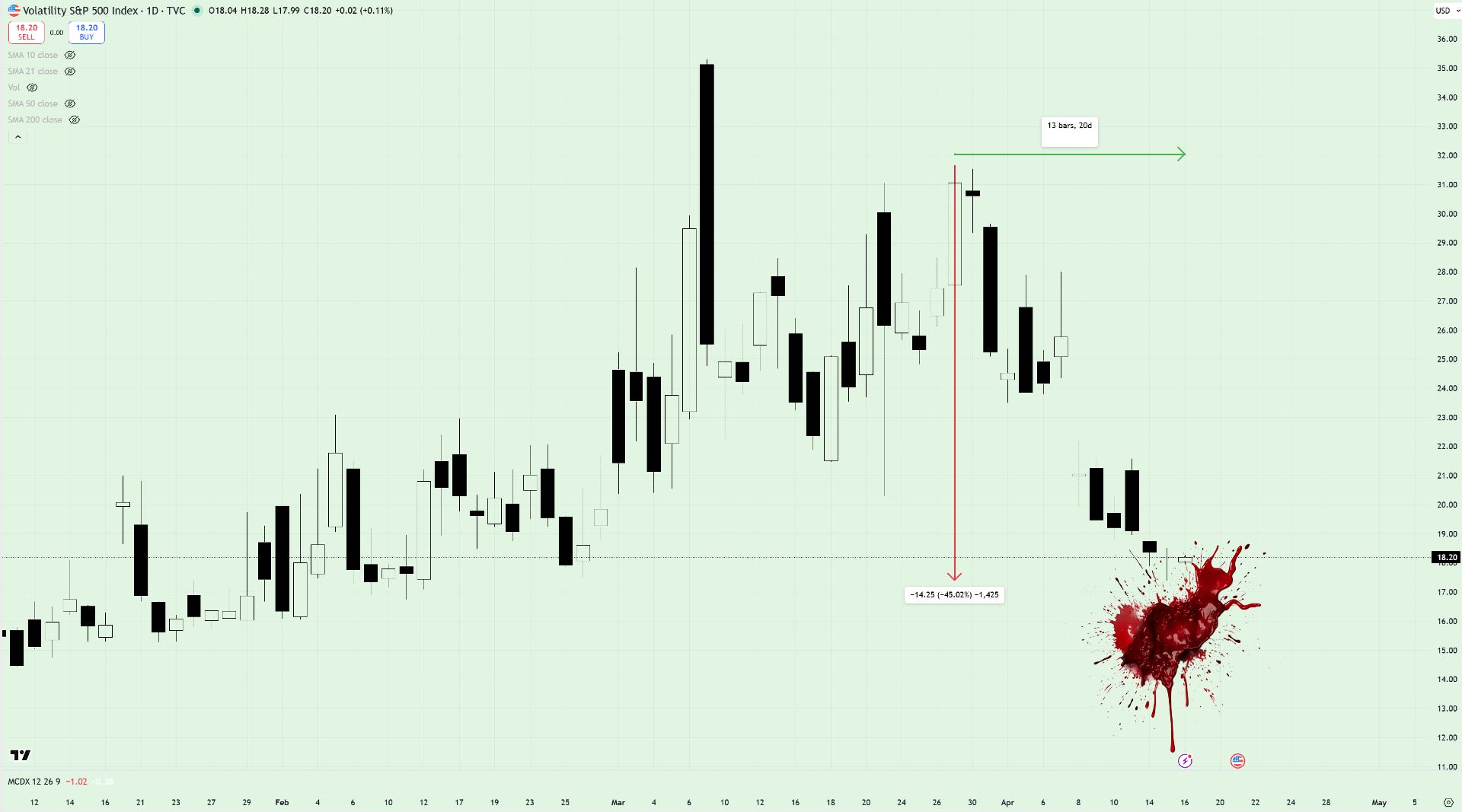

And the VIX? Stomped. Blood on the streets.

Here’s what that moment actually looked like under the hood:

SPY −10% correction → +11.2% in 11 sessions

VIX: 45 days above 50dma → sub-18 in two weeks

The third largest two-week vol compression on record

Stomp, Stomp, Stomp

We all know what commentators said the catalyst was.

If price action was Derek dragging the thief across the pavement, the de-escalation in the Middle East was the curb the bears were forced to bite down on.

That might sound overly neat. Maybe even a little narrative-heavy.

But let’s be honest - that’s exactly what many bears were doing in the weeks leading up to it. Taking a single storyline - oil up = stocks down - and running with it as if the rest of the tape didn’t exist.

And it wasn’t just wrong.

It kept them wrong long enough to miss the entire move that followed.

Because in the run-up to the de-escalation, the real warning signs weren’t only coming from oil. They were coming from the market’s internal risk gauges - the stuff that quietly flips long before positioning does.

The exact metrics I’ve been pounding the table on for weeks…

The VIX was holding above its 50-day moving average

TLT/SPY was trading above its 50-day moving average

XLP/XLY had pushed above a rising 50-day moving average

Even before a bomb was dropped on Iran, these classic risk-off signals were firing like an IED - clear enough for anyone willing to look.

And when those signals started to unwind, the outcome shouldn’t have surprised anyone paying attention.

Being Wrong ≠ Staying Wrong

I’m not going to sit here and tell you that I played the move perfectly.

But what I will say is that when my risk models gave the all clear - something which was communicated the day it occurred - I dropped the bearish thesis immediately, because when the data changes, the job is to change with it.

That’s just my approach.

I don’t build risk models for fun. I build them to help visualize the environment we’re trading in at any given moment - and more importantly, to stop myself getting anchored to a narrative once the tape has already moved on.

And that’s the difference.

Because while some traders were still leaning on the oil up = stocks down storyline, the market had already started switching regimes under the surface.

Risk signals were unwinding. Volatility was compressing. Leadership was stabilizing.

If you stayed short because the headlines still sounded bearish, you weren’t trading the market anymore - you were trading the story. And as anyone holding puts over the last fortnight will tell you, stories don’t pay. Only price does that.

What Happens Now?

Whilst bearish takes relating to inflation, negotiations or a single weak bond auction will likely crop up like mines in the Strait over the coming weeks, I’m happy following the same system that helped me tighten up in March and push down hard in April.

Should risk models flip to the downside, then you’ll be first to know - and most of the below will be invalidated in an instant. But until that happens, I’m comfortable buying some long dated positions in some of the market’s more beaten-up - and if we’re being honest, mispriced - names here.

Software

Few sectors have been hit as hard as software over the last six months. The sell-off hasn’t been selective, dragging revenue machines like MSFT down alongside weaker, story-driven names like ASAN - which is precisely where the opportunity sits.

When markets de-risk in a hurry they rarely separate quality from speculation, which means the same move that punished fragile balance sheets also reset entry points in the companies most likely to lead when conditions stabilise.

Names I like in this space: VEEV, MSFT, CRWD, INTU, PAYX

Crypto

Like software, the crypto ecosystem found itself in the grips of a brutal winter sale during Q4 2025 and Q1 2026. If risk-sentiment returns to the space - likely lead by Bitcoin resolving above $80k - then there are a good number of names to keep an eye on.

There’s still work to do, but if COIN breaks $225 and MSTR recaptures $150, it likely means game-on as far as crypto is concerned. Keep an eye on SOL and ETH too.

Semis

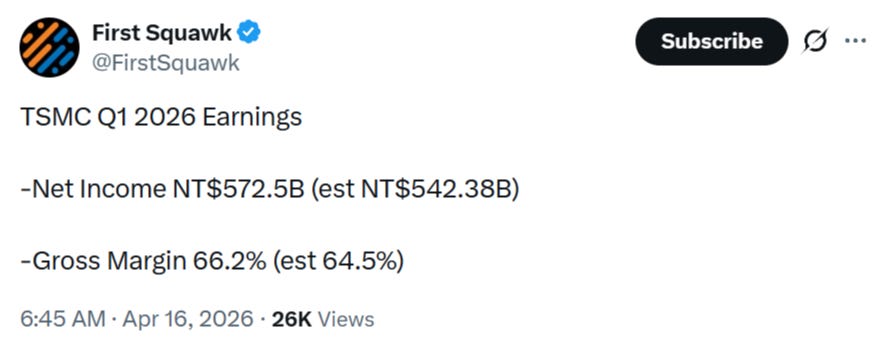

TSMC reported earnings before today’s open, once again smashing estimates and raising guidance. Sure, we’re early into earnings season - but if this sets the tone for what’s to follow from the likes of AMD and ALAB, there’s reason to remain optimistic when it comes to semis.

Data Centers

Some of my favorite names right now exist in the data center space - areas which held up surprisingly well during a turbulent Q1. Names to watch out for here include RIOT, CIFR, IREN and NBIS - just a few that are staging breakouts at the time of writing. Well worth a look in my opinion.

Financials

What if private credit fears were a nothing burger and financials - I’m talking big banks here - continue to show solid earnings growth and forward guidance? What if credit spreads remain tight and rates fade from the highs - helping the likes of JPM and C to maintain healthy balance sheets?

It’s a move I’ve been keeping an eye on for some time and it probably won’t happen overnight, but with long-dated calls locked and loaded, I’m not betting against a KBE comeback here.

Homebuilders

Homebuilders love low interest rates given the obvious correlation them and mortgages. Should rates calm a little - which could occur in lockstep with fading growth fears as a result of Middle Eastern de-escalation - then I think the likes of LGIH and PHM will resolve higher from key support levels.

FOMO, Here?

When stocks rip higher like they have over the last two weeks, it’s easy to look at charts up 10–20% - or even 50% (Ascent Solar Technologies, anyone?) - and feel like you’ve missed the move.

I know the feeling well. But the reality is that even in strong impulsive advances, pullbacks are part of the process. And as long as those setbacks happen while the under-the-hood metrics - and most importantly, my risk models - remain in the clear, I’ll treat them as opportunities to add as opposed to reasons to step aside.

Because that’s the thing about moves like this - they don’t just change price, they change positioning.

And in American History X, the curb-stomp scene isn’t the end of Derek’s story. He’s the one who ends up paying for it, and he’s the one who eventually walks out of prison seeing the world differently.

Markets have a way of doing the same thing.

Sharp regime shifts punish the narratives that overstayed their welcome. And if the last two weeks have done anything, they’ve forced a rethink from anyone still anchored to the idea the bull market is over.

Best,

Alex